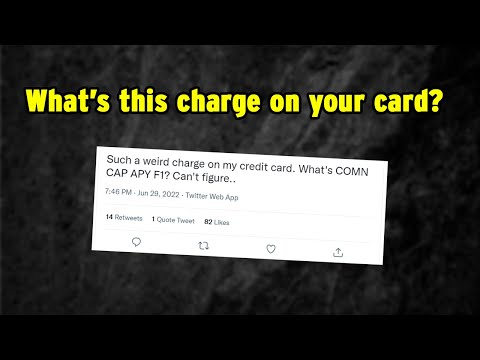

Are you looking for What Is Common Cap APY F1 Charge On Bank Statement? When you look at your bank statement, you may come across a charge labeled Common Cap APY F1. This charge is often perplexing, leading many to wonder what it means and why it appears in their statement. In this article, we will delve into the details of this mysterious charge and help you understand its implications.

Key Takeaways

- Common Cap APY F1 is often an auto-payment charge.

- It is usually associated with Comenity Bank.

- Understanding this charge can help you manage your finances better.

What Is Common Cap APY F1 Charge On Bank Statement?

The Common Cap APY F1 Charge is typically an auto-payment that is set up through a financial institution, most commonly Comenity Bank. This charge is usually related to a store service or a credit card that you own.

How Does It Work?

This charge is usually an automatic payment that gets triggered based on a pre-set schedule. When you set up an auto-payment with a financial institution like Comenity Bank, you typically agree to have a specific amount deducted from your bank account or charged to your credit card at regular intervals.

This could be monthly, quarterly, or annually, depending on the terms of the service or credit card you are using.

For example, if you have a store credit card managed by Comenity Bank, the Common Cap APY F1 Charge could be the automatic payment for your monthly credit card bill. It’s set to occur without requiring manual intervention each time, making it convenient for those who don’t want to go through the hassle of making manual payments.

However, it’s crucial to monitor these charges closely. Since they are automatic, you might forget about them and get surprised when you see the deduction on your statement. Therefore, understanding how this charge works can help you manage your finances more effectively.

How to Identify This Charge?

- Check the Statement : The first step in identifying this charge is to carefully review your bank or credit card statement. Look for a line item that specifically mentions “Common Cap APY F1” or a similar code. This is usually listed in the transactions section of your statement.

- Contact Customer Service: If you’re still unsure about the charge after reviewing your statement, the next step is to contact your bank’s customer service for clarification. They can provide details about the transaction, including the merchant’s name, transaction date, and amount.

- Review Auto-Payments: Another way to identify this charge is by reviewing your auto-payment settings. If you have set up automatic payments for a service or a credit card, especially one managed by Comenity Bank, this could be the source of the charge. Check your auto-payment settings in your bank’s app or website to confirm.

How to Manage This Charge?

- Review Statements: The first and foremost step in managing this charge is to regularly review your bank and credit card statements. Make it a habit to go through your statements at least once a month to spot any unfamiliar or unexpected charges, including the Common Cap APY F1 Charge.

- Set Up Alerts: Many banking apps and websites offer the feature to set up alerts for specific types of transactions. Utilize this feature to receive real-time notifications whenever a charge like Common Cap APY F1 appears on your account. This will allow you to take immediate action if needed.

- Consult Financial Advisor: If the charge is significant or if you find multiple instances of it that you cannot account for, it may be beneficial to consult a financial advisor. They can provide expert advice on how to manage these charges and may help you set up a financial plan to better control your expenses.

How to Dispute the Common Cap APY F1 Charge?

- Contact Your Bank: The first step in disputing the charge is to immediately contact your bank’s customer service. Most banks have a specific time frame within which you can dispute a charge, so it’s crucial to act quickly. Provide them with all the details of the charge, including the date it was made, the amount, and why you believe it’s incorrect or unauthorized.

- Gather Evidence: Before formally filing a dispute, gather all the evidence you can to support your case. This could include previous bank statements, email correspondence, or any other documentation that shows you did not authorize the charge.

- File a Dispute: Once you have all your evidence, you can proceed to file a formal dispute. This usually involves filling out a dispute form provided by your bank, either online or in a physical format. Submit the form along with any supporting documentation.

- Follow Up: After filing the dispute, make sure to follow up regularly with your bank to check the status of your case. They may require additional information or documentation, so be prepared to provide it.

The Legal Aspects of Common Cap APY F1 Charge

- Consumer Rights: As a consumer, you have specific rights under federal law to dispute unauthorized or incorrect charges on your bank or credit card statements. This includes the Common Cap APY F1 Charge. You usually have a limited time frame, often 60 days, to dispute a charge after it appears on your statement.

- Bank Policies: Financial institutions, including banks and credit card companies, have their own internal policies for handling disputes. These policies outline the procedures for filing a dispute, the types of evidence required, and the time frame for resolution. It’s crucial to familiarize yourself with these policies to effectively manage or dispute a Common Cap APY F1 Charge.

- Regulatory Oversight: Financial institutions like banks and credit card companies are regulated by governmental bodies such as the Consumer Financial Protection Bureau (CFPB) in the United States. These agencies provide guidelines and oversight to ensure that consumer rights are protected, including the right to dispute unauthorized charges.

- Legal Recourse: If your dispute is not resolved satisfactorily through the bank’s internal processes, you may have legal options. This could include filing a complaint with a regulatory body or taking legal action. However, legal action should be considered a last resort and is often more time-consuming and costly.

How to Avoid Future Common Cap APY F1 Charges?

- Review Auto-Pay Settings: One of the most effective ways to avoid future Common Cap APY F1 Charges is to regularly review your auto-payment settings. Make sure you are aware of all the automatic payments you have set up, especially those associated with financial institutions like Comenity Bank.

- Set Up Notifications: Enable transaction notifications on your banking app or website. Most financial institutions offer the option to receive real-time alerts for specific types of transactions, including auto-payments. By setting up these notifications, you’ll be alerted immediately when a Common Cap APY F1 Charge or similar transaction occurs, allowing you to take timely action if needed.

- Regular Monitoring: Consistently monitor your bank and credit card statements. Make it a habit to review your statements at least once a month to identify any unfamiliar charges, including the Common Cap APY F1 Charge.

- Cancel Unnecessary Auto-Payments: If you find that you have auto-payments for services you no longer use or need, take the time to cancel them. This will prevent future charges from appearing on your statement.

- Consult Customer Service: If you’re unsure about how to manage or cancel an auto-payment, don’t hesitate to contact customer service for guidance. They can walk you through the steps and ensure that you’re not charged in the future.

Conclusion

Understanding what the Common Cap APY F1 Charge is can help you better manage your finances and avoid any surprises in your bank statement. It’s crucial to regularly review your statements and be aware of any auto-payment setups you have, especially those managed by financial institutions like Comenity Bank.

Top FAQ’s

What is Comenity Bank?

Comenity Bank is a financial institution that often manages store credit cards and other financial services. They are commonly associated with the Common Cap APY F1 Charge.

How do I contact Comenity Bank?

You can contact Comenity Bank through their customer service number, usually found on their website or on your credit card.

No, while it is commonly associated with Comenity Bank, other financial institutions may also use similar codes for auto payments.

Can I cancel the Common Cap APY F1 auto-payment?

Yes, you can usually cancel the auto-payment by contacting the financial institution or through your bank’s app.

Are there any fees for disputing a Common Cap APY F1 Charge?

Fees for disputing a charge depend on your bank’s policies. Always check the terms and conditions.

A multifaceted professional, Muhammad Daim seamlessly blends his expertise as an accountant at a local agency with his prowess in digital marketing. With a keen eye for financial details and a modern approach to online strategies, Daim offers invaluable financial advice rooted in years of experience. His unique combination of skills positions him at the intersection of traditional finance and the evolving digital landscape, making him a sought-after expert in both domains. Whether it’s navigating the intricacies of financial statements or crafting impactful digital marketing campaigns, Daim’s holistic approach ensures that his clients receive comprehensive solutions tailored to their needs.

Related posts:

Are Credit Card Skins Legal? All You Need To Know

Are Credit Card Skins Legal? All You Need To Know

My Chime Direct Deposit Is Late [All You Need To Know]

My Chime Direct Deposit Is Late [All You Need To Know]

Does Grubhub Accept Visa Debit Cards? Quick Answer

Does Grubhub Accept Visa Debit Cards? Quick Answer

Can I Rent A Car With A Chime Debit Card? [Learn The Facts]

Can I Rent A Car With A Chime Debit Card? [Learn The Facts]

How To Add Venmo Card To Apple Pay Without Card? 4 Steps

How To Add Venmo Card To Apple Pay Without Card? 4 Steps

Can I Become A Social Worker With A Business Degree? Answered

Can I Become A Social Worker With A Business Degree? Answered

Which Is A Characteristic Of A Business Opportunity? Answered

Which Is A Characteristic Of A Business Opportunity? Answered

What Bank Is PayPal On Plaid? A Complete Breakdown

What Bank Is PayPal On Plaid? A Complete Breakdown